Author Archives: Cathy

Winning at Tennis and Markets

Stocks are like tennis: Even having just a marginal winning percentage can lead to long-term success.

Click on the link below – choose the Individual Investor Option- to watch a video of what Dimensional have to say about investing being like tennis and how over Roger Federer’s 25-year career he won 103 singles titles. He did that by winning a little more than half the points he played.

https://www.dimensional.com/au-en/insights/winning-at-tennis-and-markets

SHARE THIS POST

Planning to Downsize Your Home

When clients are outlining their funding plans for retirement, downsizing their home to release some funds is frequently part of their future strategy. Often though, by the time they are ready to make that move they do not want to leave their local friends and networks and simply want a property in a similar location that is perhaps more modern and easy-care. However, they are not alone in that search and the perceived cash release is often not there. Having a plan and building up some wealth over and above your home equity helps build greater choices down the track.

Planning to downsize your home? Not so fast

Story by Susan Edmunds Stuff 10.10.2024 Copyright © 2024, Radio New Zealand

Many New Zealanders plan to downsize from big family homes when they reach retirement – but it sometimes proves harder than expected.

It’s an issue that has been highlighted by the Retirement Commission, which said there was evidence people found it difficult to downsize due to a lack of appropriate properties.

Corelogic chief economist Kelvin Davidson said by comparing four-bedroom houses with two-bedroom townhouses it was possible to see which regions might, in a broad sense, be most difficult in which to downsize.

West Coast had the fewest two-bedroom homes compared to four-bedroom houses. That was followed by Waikato, where the number of two-bedroom townhouses was only 16 percent of the number of four-bedroom properties.

Bay of Plenty was third with 17 percent.

At the other end of the scale was Canterbury where there were more than 40 percent the number of two-bedroom houses compared to four-bedroom. Hawke’s Bay was second with 38 percent and Southland third with 36 percent.

Davidson said the bigger regions tended to have a more diverse housing stock and be easier to downsize in.

“Waikato and Bay of Plenty are at the other end of the spectrum, they are big regions with big centres but there is always an exception to the rule… Waikato has a large share of lifestyle properties and fancy suburbs with bigger sections.”

“We’ve seen clients who planned to sell a $1.5m four-bedroom home. They wanted to buy a smaller apartment. They bought a smaller apartment … but it still cost them $1.3m. Because they wanted a higher quality apartment.”

Some people expected to move to a smaller town, he said, but that could be hard if they did not want to leave families, grandchildren or friends.

“A lot of people haven’t thought about the practicalities and trade-offs of how that works. That’s why I always encourage investors to think about building wealth outside the family home. Because then you don’t have to make the same tradeoffs.”

SHARE THIS POST

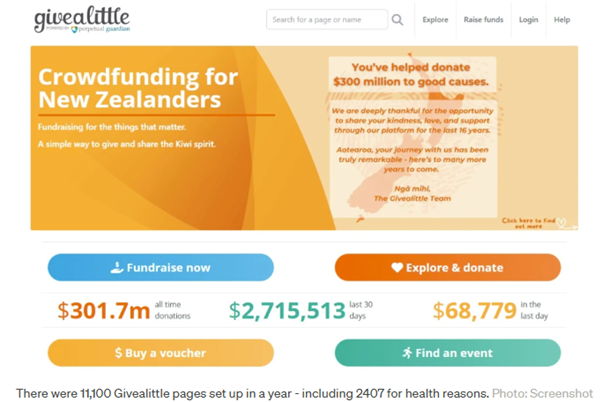

Insurance Versus Givealittle

Thousands of people turn to crowdfunding platform Givealittle every year to raise money to cover their health needs – and it’s prompted a warning from the insurance industry.

Its latest report shows there was $33.1 million donated in the year to June, of which $23.6m went to individuals.

There were 11,100 pages set up in the year. The clear majority were for health reasons – at 2407. That was followed by community causes, with 1487 and animals at 1043.

Givealittle said the number of health related pages had remained consistent over the past two years. Last year, there were 2580 such pages and the year before there were 2560.

Health causes raised $15 million in the most recent year. That could include direct treatment or living expenses and other costs related to health conditions

“The Givealittle platform can be a lifeline for those who need to raise extra funds for expensive drugs, and is an important platform to help fill the gaps where some medical treatments perhaps are not funded in NZ yet,” said Givealittle chief executive Lythan Chapman.

“We believe everyone should feel empowered to ask for help, and we’re committed to ensuring those who wish to give can do so with trust and confidence.”

Kirk Hope, chief executive of the Financial Services Council which represents health and life insurers, said Givealittle was sometimes used in cases that could have been covered by insurance.

“What we’ve seen with the economic downturn is people are not really assessing risk. They are saying we can’t afford certain things, they might say that health insurance for example is discretionary… then they’re having to rely on things like Givealittle for support.”

He said people needed to take care before cancelling insurance to understand what they could face if their health circumstances changed.

“The last place you want to be relying on is others through things like Givealittle.”

He said New Zealand needed to get public policy settings right so that employers who wanted to offer insurance to staff could do so easily.

“Fringe benefit tax could be looked at. It needs to be looked at from a macro perspective, there are a few things we might want to change to enable and incentivise people so they can take up insurance to cover themselves so they’re not relying on Givealittle.”

Article by

Susan Edmunds, Money Correspondent RNZ

SHARE THIS POST

Recent Changes to KiwiSaver Scheme Rules

Following the changes to the KiwiSaver Scheme contribution rules announced in the most recent Budget, we have made some commentary here, particularly for those of you who are self-employed earning over $180,000, where the government contribution will cease.

The full changes are:

- The government contribution is being halved to 25 cents for every dollar a member contributes year, up to a maximum of $260.72. Currently, where a member contributes $1,042.86 pa, the government contributes $521.46. From hereon the minimum contribution of $1,042.86 is still needed to be made by the member (either via voluntary contributions or employee payments) to get the reduced $260.72

- The default rate of employee and employer contributions will rise from 3% of salary to 4% in two steps. From 1st April 2026 the rate will go up to 3.5%, and from 1st April 2028, it will increase to 4%. The increases are being phased in over a three year period to help workers and employers plan ahead

Employees will have the option to roll their contribution rate back down to the 3% rate and their employer can then match it at that lower rate, too. This will be a temporary option if, for example, they feel they are unable to afford the increased contribution for a period of time

- Members with an income of more than $180,000 pa will no longer receive the government contribution from 1st July 2025

- The government contribution is being extended to include 16 and 17 year olds from 1st July 2025, and employers will have to contribute to these age groups too from 1st April 2026

For any of you who are self-employed earning over $180,000 pa, who have been contributing the minimum regularly to receive the government contribution, you may now be asking yourself if you should stop your contributions as you will no longer receive the government credit?

We have the following comments that you might want to consider:

- If you stop your contributions, what else are you going to do with those funds? Where will you redirect them to in order to support the growth for your retirement savings?

- If you redirect them to other growth investments for the longer-term, where this money may not be locked-in, that could be a good thing. However, be mindful that not having any ‘lock-in’ means that you need to be disciplined in leaving this money to grow for your retirement, as it can be tempting to access it sooner than ideal, for other spending needs

- As the existing balance cannot be accessed until age 65, continuing to contribute into a quality investment portfolio will help grow a ‘pot of money’ that will be useful for you in retirement. Do bear in mind however, that whilst the rules currently say KiwiSaver Scheme money can be accessed at age 65, this may change if the government increases the age of eligibility

- Whilst it is disappointing to have lost the government contribution, when focussing on your wider plans to grow your wealth for your retirement years, continuing on saving may be the wise choice

If you wish to discuss your own particular circumstances, please feel free to reach out to us.

Charlene Overell

G3 Financial Freedom

SHARE THIS POST

On The Road to a Successful 2025

As 2024 comes to a close, it’s the perfect time to take a step back and evaluate your financial situation in preparation for a successful 2025. By checking in on your finances now, you’ll ensure you’re in a strong position to reach your goals in the year ahead and beyond, with the aim of living your best life.

For a reminder of some key areas to review as we head into the new year take a look at our checklist below:

1. Personal Insurances

If you’ve increased or decreased debt, changed jobs or had a pay rise, bought an investment property, sold one, grown your family or had any other major changes in life, then it’s important to check your personal insurances such as Life, Income Protection and Trauma cover, have been adjusted to suit your new circumstances. This is about providing the right money to the right people at the right time.

2. Check Your Estate Planning Documents

Estate planning is often overlooked but it’s essential for protecting your assets and ensuring your wishes are carried out as part of your legacy, so make sure to:

- Review your Will and Trust Documentation – Are they up to date? Do they reflect your current family and financial situation?

- Review the beneficiaries listed and other financial documents to make sure they reflect your wishes.

- Check your Enduring Powers of Attorney (EPA) – make sure the people you have appointed are still appropriate for both Property and Care & Welfare

- If you don’t have either a Will or EPA – make it your New Year’s resolution to establish these as soon as possible, as without an EPA, if anything were to happen and one is needed, it can costs thousands to apply to the Court to have someone appointed (who may not be who you’d choose!)

3. Review Your Expenses and Savings for 2025

A fresh start in 2025 means keeping a close check on your spending – we’re all aware that costs have increased significantly over the last couple of years and it’s good to be on top of things.

- Review your spending – If you’re in the accumulation phase of life, trying to build up your savings and investments, look at your spending habits over the past year and identify areas where you could potentially find some savings instead of possibly ‘frittering’ money away

- If you’re retired – let us know if the income you’re getting from your investment portfolio is now feeling ‘tighter’ than before, and not covering your costs, or perhaps there are things on your bucket list you still want to do while you can!! Part of our role is to give you permission to spend your money whilst providing you with peace of mind that you’re not going to run out of it

- Make sure you have an emergency fund in cash – Having a cash fund helps take the pressure off when something unexpected but costly happens, such as a major car bill, a period of being unable to work etc. We suggest you try and set aside 3-6 months of your expenses in a ‘rainy day’ fund

- Set new financial goals – Whether it’s saving for a big purchase, paying down debt, or investing for the future to ensure you have a comfortable and secure retirement, having a goal can help drive success. If you’d like our support with helping define what’s important to you, please get in touch

4. Mortage Payments

Check-in on what your current mortgage interest rate is, what your payments are, and if you need to make any changes.

- If you’ll be re-fixing in 2025 – then with interest rates dropping, try to maintain your payments at the higher level to help clear your mortgage sooner

- If you have any high interest debt on credit cards or such – these should be repaid as a priority

5. Retirement Savings and Investments

Revisit the savings you’re making, what investments you have in place, and where these are being invested.

- Review your KiwiSaver Scheme – it’s easy to let this run along in the background, and when markets are volatile, which is normal by the way and to be expected, this is ‘okay’ provided you’re in the right fund for your situation, so take the time to look at your fund choice

- Review any other long-term savings – check on your investment strategy to ensure it aligns with your long-term goals, risk tolerance and any ‘ethical’ preferences you may have of wanting to invest in a socially responsible way. Revisit the level you’re able to save and whether you’re on track for the money you’ll need to spend in the future

6. Preparing for a Prosperous 2025

By reviewing and updating these key areas of your financial life you’ll be better positioned to take control of your money for 2025. Starting the year with a clear financial plan can help reduce stress and set you up for success. As always, we’re here to support you, so please feel free to reach out.

Wishing you a smooth end to 2024 and a prosperous 2025!

SHARE THIS POST

Charlene – Volunteer of the Year 2024

It was with great surprise and delight that Charlene was awarded Volunteer of the Year 2024 by Financial Advice New Zealand, her professional body. Charlene enjoys ‘giving back’ and has been a member of several committees within Financial Advice New Zealand and other organisations all throughout her career.

Charlene believes in championing quality independent advice within the financial planning profession, and providing advocacy where she can. She feels that she ‘gets back more than she puts in’ and just enjoys working with her colleagues and being the best support she can.

To paraphrase Charlene’s comments after receiving her award:

“To be recognised by my peers within our profession is quite special, and I’m very grateful for their support, especially as it’s the people around me and on those committees that have made my input enjoyable and fun!”

“For me, sharing knowledge and imparting wisdom I’ve picked up during my career hopefully helps in some small way to empower others to join this profession and continue their career path. There’s always something new to learn so we can be and do better.”

“We get to understand our client’s values and they share so much with us, so being in a position of trust to help make a positive difference in their lives, providing them with peace of mind and security around what’s important to them, is a privilege and an honour.”

SHARE THIS POST

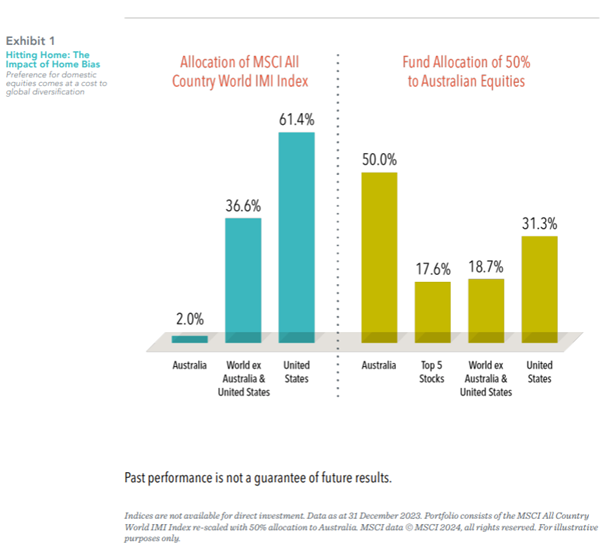

Investing: The Case For Leaving Home

While it’s true that there’s no place like home, when it comes to investing there are costs

involved in being too chained to your own patch.

Australians and New Zealanders, like investors everywhere, tend to have a home bias in

their portfolios. And there can be rational reasons for this in the tax advantages of

dividend imputation or merely their familiarity with local stocks.

However, too large a home bias may have undesirable consequences, in leaving

investors with concentrated exposures to individual companies and sectors and in turn

missing out on the opportunities from exposure to sectors not well represented in the

local market. The concentration trade-off in Australia is magnified by the large market

share of a handful of companies.

Highlighting the degree of potentially lost opportunity, stocks of the roughly 18,000

companies trading outside Australia represent about 98% of the world’s more than $120

trillion equity market.

Yet, it is not uncommon for some local investors to have a 50% allocation to Australia. In

other words, half of their equity portfolios are in a market that represents just 2% of the

global market. In the case of New Zealand investors with a similar home bias, the

concentration is even more pronounced.

To put this in context, a portfolio with a 50% allocation to Australia has just five stocks

(BHP Billiton, CSL and three of the big four banks) holding a weight roughly equivalent to

all the stocks outside of Australia and the US. Just to be clear, this means that just five

stocks in such a portfolio will have more weight than 46 markets with more than 15,500

companies!

When Australians and New Zealanders invest outside their home markets, they can

capture equity returns from thousands of companies around the globe and potentially

offset weak performance in one market with stronger returns elsewhere. In other words,

holding a globally diversified portfolio positions investors to capture returns wherever

they occur.

This material is issued by DFA Australia Limited (incorporated in Australia, AFS License No. 238093, ABN 46 065 937 671). This material is provided for information only. This material does not give any recommendation or opinion to acquire any financial product or any financial advice product, and is not financial advice to you or any other person. No account has been taken of the objectives, financial situation or needs of any particular person. Accordingly, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. Investors should also consider the Product Disclosure Statement (PDS) and for the Dimensional Wholesale Trusts the target market determination (TMD) that have been made for each financial product or financial advice product either issued or distributed by DFA Australia Limited prior to acquiring or continuing to hold any investment. Go to dimensional.com/funds to access a copy of the PDS or the relevant TMD. Any opinions expressed in this material reflect our judgement at the date of publication and are subject to change.

Article by

Warwick Schneller, PhD

Senior Investment Strategist and Vice President

Dimensional

SHARE THIS POST

The Importance of Reviewing Your Personal Insurances

For the majority of us, when the renewal notice for our personal insurance policy arrives, it is an eye-rolling event. Invariably the regular premium increase further fuels the feeling that insurance is a necessary evil – something that we know we need to have but would rather not pay for.

The world of Personal Insurance which includes Life, Income Cover, Trauma (Critical Illness) and disability insurance, alongside Health (or medical) cover has become complicated. There are lots of permutations as to the depth of the cover and there are various additional bells & whistles that can be added to a policy for added benefits on a claim.

We believe there is a hierarchy of needs when it comes to insurance and work with clients to ensure that their covers suit their personal situation – this is not a set and forget solution though and so it is important that your policy is reviewed regularly to make sure it has kept up with your changing situation.

Dependents and Financial Obligations: If you have family who are depending on your income and if you have debts then life insurance should be a top priority

Income Stability: If your income is essential for maintaining your lifestyle, paying your mortgage etc. then income protection insurance is crucial

Health Risks: to protect against serious illnesses or permanent disability, trauma and total & permanent disability insurance can provide peace of mind by providing a lump sum which could reduce debt, replace income or pay for some medical treatment

Healthcare Costs: Medical insurance helps you get the treatment you might need when you need it

Generally, it is not in your best interest to change your existing policy provider as you get older, unless there is a specific reason why the current cover is no longer adequate, as your health has probably changed over the years. But there are often some ways you can increase your existing cover to reflect your changed circumstances without having to have a new health assessment. Examples might be an increase in your debt, marriage, divorce, birth of a new child, or a pay-rise and so it is important that you meet for a review regularly to assess what might be needed as there are time limits applied to have an increase without proof of health.

Chasing cheaper premiums is also not a viable course of action as the cheapest on the market today might not be tomorrow. Knowing that the insurer will pay a claim if needed, and that you have some of the best policy wording available for any specific areas important to you, is a better way of choosing your insurer.

If you do suffer some kind of medical incident, let us know! It is surprising the number of people we catch up with who casually mention they were in hospital or broke a wrist and their particular policies meant that we could claim a small benefit for them.

Of course, keeping insurance premiums affordable is important and we will do our best to work with any constraints you have to help you have the most suitable cover within your means however, it might be useful to understand the factors that influence premium pricing, particularly for Health (Medical) policies.

Age as we get older our risk of claiming, particularly on medical policies, increases

Medical Inflation: This is a significant driver. Medical inflation refers to the rising costs associated with medical procedures, medications, and technologies. As medical treatments become more advanced, they also become more expensive.

Preventative Care: There is a greater availability of preventative care options and testing, which involves clients receiving more frequent screenings and diagnostics.

Reinsurance Costs: The cost of reinsurance, which is insurance for insurance companies, has been rising

Whilst in an ideal world none of us want to claim on a personal insurance policy, at G3 we also see the difference a claim can make by removing any financial stress or having treatment privately rather than having to wait in the public system. Knowing you have the right cover can provide a real sense of security.

We email you every year with your updated schedule, offering a review – please make sure you take advantage of this, particularly as life changes and it is in your best interest that we know what has been happening.

Article by Jane Benton

G3 Financial Freedom Ltd

SHARE THIS POST

Rethinking Retirement

The concept of retirement has changed considerably in the last 143 years.

In 1881, Otto von Bismarck, the conservative president of Prussia, presented a revolutionary idea to the Reichstag – that the government should provide financial support to older members of society. In other words, a government sponsored retirement. The idea was radical because, back then, people simply didn’t retire. If you were alive, you probably worked on a farm; or if you were wealthier, you might have managed a farm or larger estate.

But von Bismarck was under pressure from socialist opponents to do better by the people, so he argued that “those who are disabled from work by age and invalidity have a well-grounded claim to receive care from the state.” It would take another eight years to bring this to fruition, but by the end of the decade the German government would create a retirement system which provided for citizens over the age of 70, if they lived that long. The qualifying age subsequently reduced to 65 in 1916.

In New Zealand, public pensions did not exist until 1898. At that time, the relatively small numbers of elderly pakeha were expected to provide for themselves or be supported by their families, and older Māori were supported in the traditional way by their whanau.

However, by the late 19th century the number of poor elderly in New Zealand were growing and this sparked vigorous political debate on the appropriate government response. This resulted in an Old Age Pension being introduced in 1898. Those aged 65 plus could apply but were subject to a rigorous means test that covered both income and assets.

At the time, of course, many potential pensioners did not make it to age 65, which meant the financial burden on the state was relatively modest. But by the turn of last century, demographic trends began changing, and what was seemingly smart politics in 1898 looks more problematic in 2024.

In New Zealand today, if you reach the age of 65 in good health, on average you can expect to live another 23 years (male) to 25 years (female). This means von Bismark’s original idea of providing financial support in the unlikely event you lived long enough to need it, has become an increasingly heavy burden on western governments the world over. Particularly for those governments (like New Zealand’s) who have been slow to adjust their retirement systems in the face of a trend towards greater longevity.

With people living so much longer these days, the whole notion of retirement has also changed. A vague plan might have been something like – work for 40-50 years, then have a retirement party, get a gold watch, and get ready for an exciting 25 years or so of golf.

Rather than jumping from full-time work into full-time retirement at age 65, the answer for many lies in planning more creatively for other options later in life. This could involve scaling work back to some degree (but not immediately to zero) or even changing careers around 55 or 60, but still working for another 15 or 20 years in some capacity.

If you can find a way to extend your working life by a decade or more, even with part-time work, you give your retirement savings that much longer to grow. It’s not uncommon for people to “retire” from jobs they dislike earlier than they thought financially possible. This can work wonders for your stress levels and quality of life, as long as the income from your substitute job is enough to cover regular expenses.

Often, these ‘retirees’ can’t keep saving for their retirement fund to the same extent as before, but, more importantly, they won’t need to dip into their retirement nest egg either. Don’t underestimate the effect of another decade of compound growth on your investments at that point in your life – it’s incredibly powerful.

Today, retirement can be 25 to 30 years or more. And over that period, the likelihood that inflation eats away at your purchasing power is a much more serious threat. Based on a 3% annual inflation rate, the purchasing power of one dollar today reduces to just 50 cents after 23 years and to 40 cents after 30 years. This means the financial risk embedded in living a long and healthy retirement is that your savings are going to need to do more, and for longer.

The real financial risk is the potential for you to outlive your assets. That’s why rethinking your investment plans and your late-life workplans could form part of a practical new-age retirement solution that von Bismark could never have contemplated.

For many people, retirement is the light at the end of a tunnel called a career. How about flipping that paradigm on its head so that the end goal isn’t to stop doing the wrong kind of work, but to start doing the right kind of work?

With that mindset, just imagine how enjoyable those later working years could be. Or maybe that long-awaited retirement party and the gold watch will keep you satisfied for the next 25 years. And hey, there’s always golf, right?

Article by Damon O’Brien

Investment Director

Consilium

SHARE THIS POST

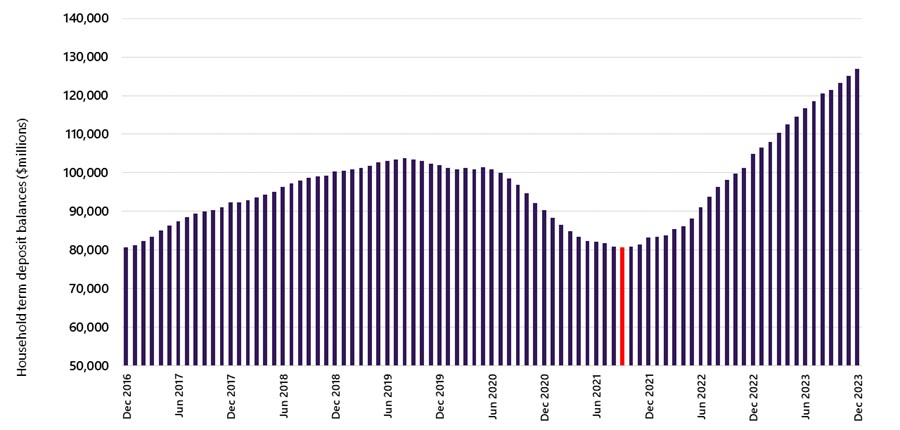

The poor plight of investors that switched from Term Deposits during COVID

It’s a little detail you may have missed, and even if you heard it, you probably gave it no more than passing attention. In December 2023, New Zealand hit an all-time high in term deposit (TD) balances of a whopping $213b1. If you look only at households (see the chart below), that number reached $127b, easily outstripping the combined balances of every KiwiSaver investor in the country.

While that huge number is interesting, what’s more interesting is the change of TD balances over time. It turns out that TD balances have not experienced a slow and steady upward climb. Instead, there was a recent peak, followed by a trough, and now we are on another peak. The low balance point, September 2021, is highlighted in red.

Household TD’s and NZX50 Growth of Wealth Dec 2016 – Dec 2023

Source: RBNZ and NZX

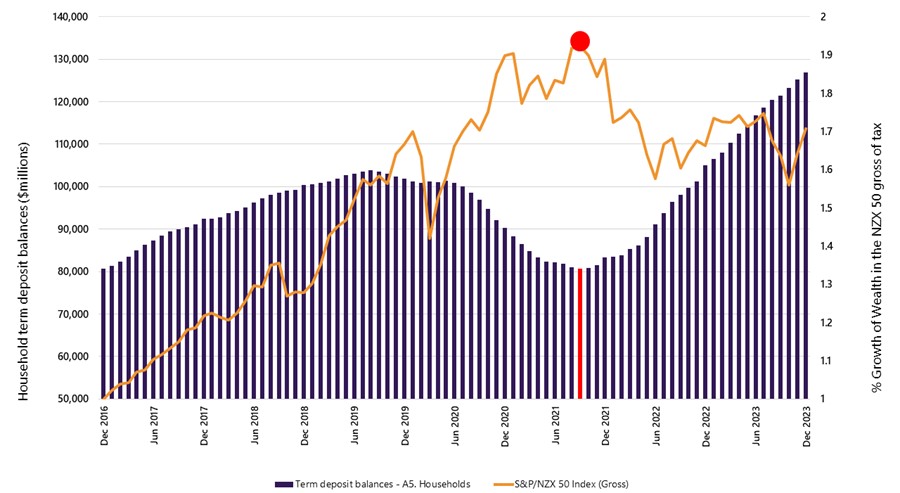

This chart shows that investors were slowly accumulating TD assets from 2016 to 2019. Then, in response to COVID, the Reserve Bank sharply reduced interest rates. Pretty soon, about $25b in TD assets started looking for something (anything) with a higher yield. At the time, investment portfolios looked like an attractive alternative based on the recent good run the market had experienced.

By December 2022, the trend (and interest rates) had reversed, and TD balances were back to setting all time highs which continued unabated in 2023.

So, what is the issue?

The issue is the remarkably bad investment timing this represents and impact it likely had on many new investors.

From 2016 – 2019 whilst TD volumes were growing steadily, the New Zealand share market measured by the NZX 50 Index (Gross) generated, on average a return of 16.10% per year. By comparison 6-month TD’s generated 3.25% per year over that same time period. Despite these unusually good share market returns, TD balances were gradually still increasing each month. In other words, TD investors were not noticeably substituting out of TDs and moving into those high performing assets during the years of great share market results.

But investors, at least anecdotally, did decide to switch from TDs to investment portfolios throughout 2021 and 2022 and TD balances hit their low point in September 2021. In other words, for investors that moved away from TDs, the date of their maximum exposure to investment markets was September 2021. Unfortunately, from that date to the end of 2022, the NZX50 returned an unwelcome -10.08% and the NZX Investment Grade Corporate Bond Index delivered -5.31%.

Following that uncomfortable investment experience, investors apparently came rushing back into TDs. And, while they did, markets recovered. Sure, the NZX was up only 2.59% in 2023, but the bond index was up 7.54% and the MSCI All Country World Index (gross div.) was up 23.35% helping investors that diversified internationally.

So, here’s the problem in a nutshell:

- A large group of TD investors appear to have missed out on the great investment markets pre-COVID.

- Disenchanted with low interest rates, they moved into investment portfolios in 2021 and 2022 searching for better returns.

- They ended up running right into bad share returns and historically bad bond returns.

- Many appear to have jumped back out of investment markets in 2023 only to miss out on the stellar bond and global investment returns that 2023 delivered to disciplined investors.

Yikes!

The graph below really shows the story. TD deposits hit their lows, right on cue when the NZX hit its high (September 2021). So, as markets go down, the maximum amount of former TD investors feel the brunt of poor returns, and they quickly move back into TD’s rather than stick around to enjoy the recovery.

We’ve highlighted September 2021 when the NZX50 was at its peak and the cumulative TD balance was at its low (the same month).

Household TD’s and NZX50 Growth of Wealth Dec 2016 – Dec 2023

Source: RBNZ and NZX

What is the lesson?

The first lesson is that as a nation we are collectively terrible at ‘timing’ markets. But we’re not alone.

In the United States one of the most esteemed investment consultants is Charles Ellis, author of “Winning the Loser’s Game.” He said this about market timing, “market timing is a truly wicked idea. Don’t try it.”

He also said, “Market timing is unappealing to long-term investors. As in hunting deer or fishing for rainbow trout, investors have learned the importance of ‘being there’ and using patient persistence – so they are there when opportunity knocks.”

For investors that started investing in 2021 only to be disappointed in 2022, our strong encouragement is to hold on and stay disciplined. It’s nearly impossible to pick the times to be in and out of the market. Instead, if their strategy needs to last over decades, then give it time and work with an adviser to see if the plan is still on track, or if they need to make some small adjustments.

Discipline and time are the super skills of great investors. It’s the one thing consistently rewarded, and something that a good adviser can help us be much better at.

1Source: Banks: Liabilities – Deposits by sector (S40) – Reserve Bank of New Zealand – Te Pūtea Matua (rbnz.govt.nz)

Ben Brinkerhoff

Consilium

08 April 2024

SHARE THIS POST

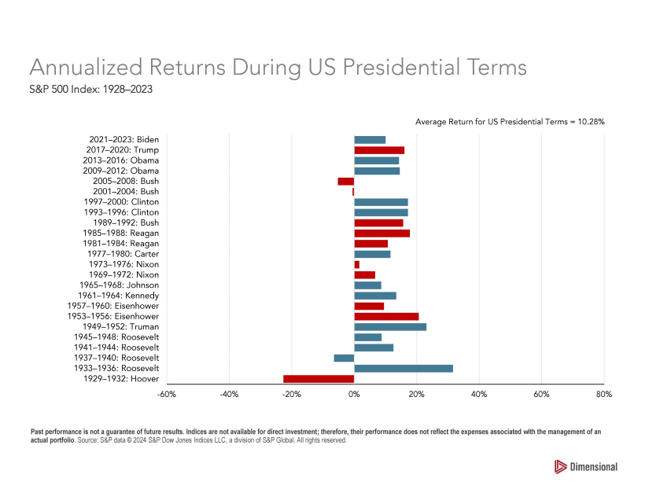

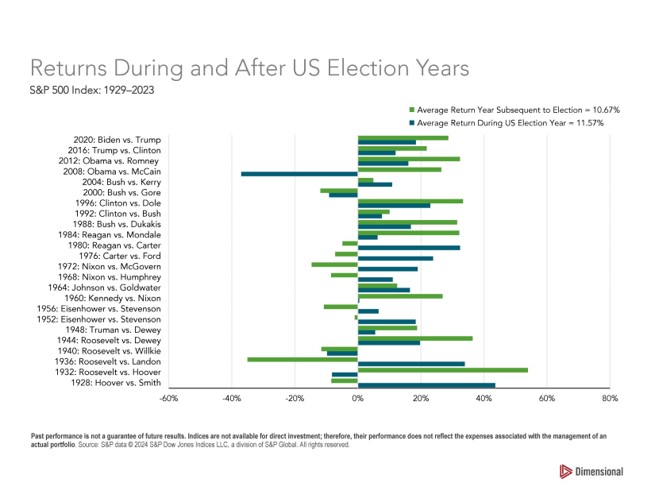

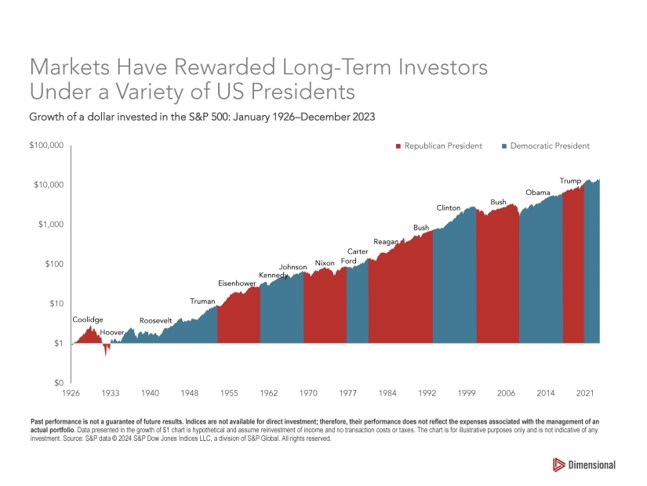

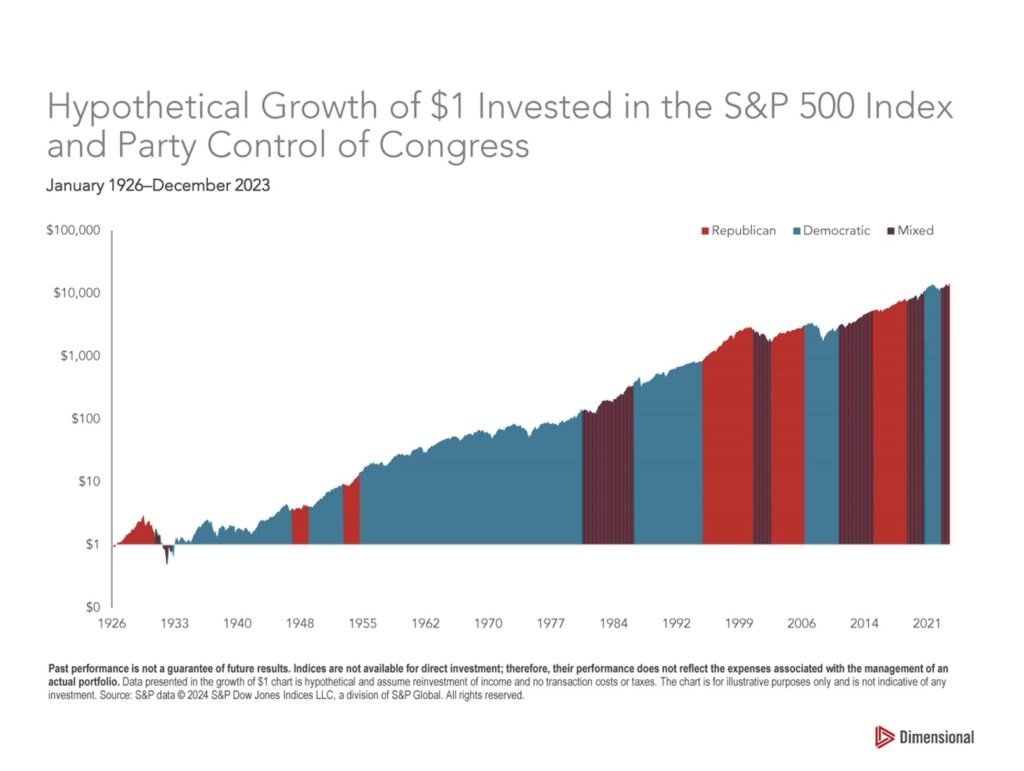

Do you wait for elections to pass before investing?

This is a question we are always asked when election time comes around, or, investors with cash to invest say “I’ll just wait to see what happens in the election and for things to settle down before I invest”.

Does waiting make any difference?

Does it matter which party ‘gets in’?

To answer these questions, we recently had a conversation with an expert at Dimensional Fund Advisers who shed some light on this topic.

Whilst the following graphs are US centric, this still applies to more local election time in New Zealand too, in that it’s unpredictable, there is no pattern, and you need to invest for your own personal goals and long term planning aims, and not get caught up in trying to guess what may or may not come about.

It’s US election time coming up, and as the US is a major area of the world portfolios are invested in, these graphs are worth taking note of and ‘just getting invested’, controlling what you can control and not worrying about what you cannot.

Lets look at history and consider the annual returns of the S&P 500 Index (the 500 leading publicly traded companies in the US) and how these have been affected by the whether the Democrats or Republicans sat in the White House

And what about the S&P 500 Index returns DURING and AFTER US election years:

As you can see, history tells us it’s futile to try to predict the future and elections have made no real difference to investment returns. Being invested ‘full stop’, and staying invested, is the best course of action to grow wealth and protect it. Trying to wait for the right time, will mean the right time never comes, and you could be looking back wishing you had taken advice around what goals you want to achieve, and just ‘got started’, at that is what you can control!

Charlene Overell

G3 Financial Freedom Ltd

05.06.2024

SHARE THIS POST

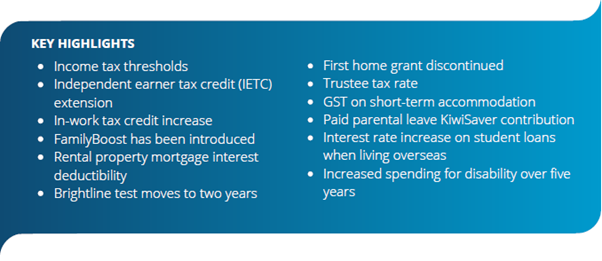

New Zealand Budget 2024

On 30th May, the New Zealand Government released the National Budget 2024. We have

shared below highlights of the Budget which may have implications to wealth creation and

retirement plans, property, and family cash flow decisions.

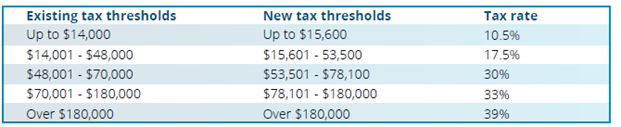

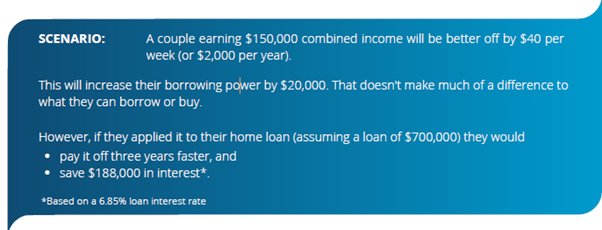

TAXATION

INCOME TAX THRESHOLDS CHANGES

The personal income tax rates thresholds increase from 31 July 2024, excluding the tax rate for income

over $180,000 per annum.

INDEPENDENT EARNER TAX CREDIT EXTENSION

The upper limit of the eligibility for the Independent Earner Tax Credit (IETC) will be extended from

$48,000 to $70,000 per annum. Those earning $24,000 to $66,000 per annum will receive the full $20 per

fortnight credit. The entitlement reduces gradually for income between $66,001 and $70,000. This is

effective from 31 July 2024.

IN-WORK TAX CREDIT INCREASE

The In-Work Tax Credit (IWTC) is a tax for families with dependent children who are normally in paid work

if the annual family income after tax is less than $35,204. The increase is up to $72.50 per week ($3,770

per year) to working families for the first three children and up to $15 extra a week for each additional

child. This is effective from 1 July 2024.

FAMILYBOOST

From 1 July 2024, parents and caregivers will be eligible for a partial reimbursement of their early

childhood education (ECE) fees, up to a maximum fortnightly payment of $150. Reimbursements will be

made quarterly, as a lump sum. The first payments will therefore be made from October.

This maximum payment slowly reduces for family incomes over $140,000 per annum. Families with

incomes over $180,000 per annum are not eligible for FamilyBoost.

PROPERTY

RESIDENTIAL PROPERTY TAX

Effective since 1 April 2024, the ability to claim interest deductions on residential property investments has been phased back in. Between 1 April 2024 – 31 March 2025, 80% of interest can be claimed. From 1 April 2025 onwards, 100% of interest can be claimed.

BRIGHTLINE TEST

The brightline test will be reduced from ten years to two years on all properties from 1 July 2024. This may bring more properties to the market as it removes a barrier to selling. The higher costs of insurance and potential raises in local council rates are detracting property investors.

The changes to the brightline test may help some investors rebalance their portfolios given the impact of the introduction of Debt-to-income (DTI) ratios limiting the ability to borrow in the future.

FIRST HOME GRANT

The first home grant has been discontinued. First home loans are still available, enabling first home buyers to only need a 5% deposit for their first house, based on eligibility criteria.

First Home Loans are issued by selected banks and other lenders, and underwritten by Kāinga Ora. This

allows the lender to provide loans that would otherwise sit outside their lending criteria.

INVESTMENT & SAVINGS

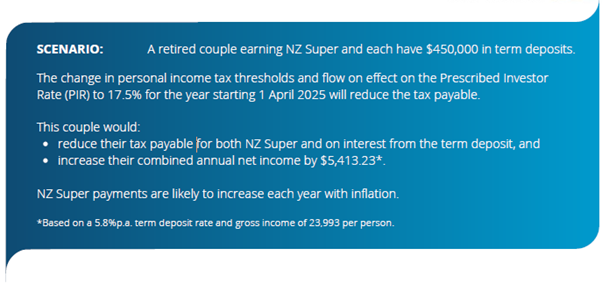

PERSONAL INCOME TAX

The changes to the tax thresholds impact other taxes, including fringe benefit tax (FBT), employer

superannuation contribution tax (ESCT), residential withholding tax (RWT) and prescribed investor rates

(PIR). Clients will need to review the implications with their financial advisers

TRUSTEE TAX RATE INCREASES

The new tax rate for trustees announced last year is effective from 1 April 2024. The trustee tax rate is

39% for the 2024-2025 and later income years. Reviewing trusts and considering using portfolio

investment entities (which have a maximum tax rate of 28%) may minimise the impact of the tax changes

GST ON SHORT-STAY ACCOMMODATION

Clients who be impacted by the new Goods and Services Tax (GST) on short-term accommodation. Online

marketplace operators must collect and return GST of 15% when the service is performed, provided, or

received in New Zealand. This applies to New Zealand and offshore operators. Holiday rental cleaning fees would also be subject to GST. Accommodation used by the customer as their principal place of residence is exempt.

A new flat-rate credit scheme will apply for sellers who are not GST registered. Marketplace operators will

collect GST at the standard 15% rate. They will pass on 8.5% to sellers who are not GST registered. The

remaining 6.5% will be paid to the Inland Revenue Department. These are excluded income for income tax purposes.

PAID PARENTAL LEAVE KIWISAVER CONTRIBUTIONS

Parents who choose to have KiwiSaver deducted from their paid parental leave payments will receive a 3%

Government contribution to their KiwiSaver fund. The contribution would be liable for employer

contribution tax (ESCT). This is effective from 1 July 2024.

NZ SUPER AND DISABILITY SUPPORT

RETIREMENT

The changes to the Personal Income Tax threshold will mean some people receiving NZ Super will get

more in hand if they’re on the ‘M’ tax code. The after-tax rate for NZ Super may increase by up to $4.30

per fortnight. No changes apply if clients are on a ‘S’ tax code.

INCREASE IN SPENDING FOR DISABILITY SUPPORT SERVICES

The government has allocated $1.1 billion over five years to ensure the Ministry of Disabled People

Whaikana can continue to deliver critical disability support services.

This funding is an addition to the government’s more than $2.2 billion per annum investment in disability

support services. The support services include home and community support services, respite care

community residential care, environmental support services, and the High and Complex Framework

Strategy.

PRESCRIPTION CO-PAYMENT

From 1 July 2024, the $5 co-payment for fully subsidised prescription items from publicly funded health

providers will return for everyone except people aged 65 and over, community services cardholders and

under 14-year-olds.

STUDENT LOANS & FUNDING

HIGHER INTEREST RATE WHEN LIVING OVERSEAS WITH A STUDENT LOAN

The Budget 2024 has introduced some significant changes to the overseas student loan system. The

interest rate charged to student loan borrowers who are based overseas will increase by 1% for five years,

taking effect from 1 April 2025. The new rate is forecast to be 4.9%.

FEES FREE SCHEME

The Fees Free Scheme for the first year of study and training will end at the end of 2024. It will be replaced with a final-year fees free scheme starting from January 2025.

APPRENTICESHIP BOOST

The Apprenticeship Boost initiative will continue with ongoing funding. From 1 January 2025, only first-year apprentices in targeted industry areas will be eligible for the $500 per month subsidy.

This information in this document is provided by Financial Advice New Zealand. It may include general information based on online government announcements and Ministry websites. It does not consider your individual objectives, financial situations, needs or tax circumstances. We recommend consulting with a financial advice professional to discuss your specific needs. Find an adviser at financialadvice.nz

SHARE THIS POST

Celebrating 15 years

This week G3 Financial Freedom has officially been in business for 15 years.

A lot has happened over that period with different faces and changes in office locations. Hopefully, the one thing that hasn’t changed is that, as a team, we continue to demonstrate the Company’s core values to you.

Our Values:

- Generosity: we aim to be generous with our time, knowledge, and experience

- Gregariousness: we enjoy what we do and want you to enjoy working with us

- Guardianship: we help you make informed decisions about protecting and growing your wealth

We don’t often share things with you in our newsletter, around what is happening with us, however this time, reaching this 15 year milestone, we feel we can look back and celebrate a few of our more recent achievements with you.

Both Charlene and Jane have continued to be involved within the wider financial services industry, serving on various committees within organisations that support financial planners nationally, advocating for independent advice, and supporting initiatives to increase financial literacy within New Zealand. We love what we do and are always keen to be a part of shaping our profession for the better and making financial advice available to all.

Ellie has completed her Post Graduate Diploma in Business Studies in Personal Financial Planning and had her proud graduation moment. This is a fantastic achievement involving a lot of hard work, juggling between being in the office and looking after her two young children whilst studying. Her next goal is to complete the steps to become a Certified Financial Planner, the pinnacle of financial planning worldwide.

Cathy continues to keep us in line, and having been with us since day one, remains the backbone of G3, providing exceptional customer service to all our clients and connections. We cannot thank Cathy enough for her cheerful support through all these years, as she runs the office and our client support services.

Whilst we each have our individual community involvements, G3 has sponsored the annual Festival of Disability Sport that takes place in Tauranga, since its inaugural launch in 2018. We’ve always attended the sessions to support the athletes, and this year, Ellie’s children, Syd and Maddie, got to try a game of wheelchair basketball! We would like to encourage anyone to check out this event (normally held in March), to support these amazing athletes, and see for themselves how inspiring these individuals can be, and to ‘have a go’ – the wheelchair rugby in particular is brutal to watch, but great fun too!!

Our success is of course dependent upon you, our clients, and our professional friends who recommend their clients to us. We have grown organically over the past 15 years and now look after close to $80million of invested funds alongside our insurance and wider financial planning clients. Our aim remains always to retain our personalised approach, knowing our clients well, and providing a first class service. Thank you for being part of our journey; we’re looking forward to more years ahead working alongside you. If you have someone you know and care about, who you feel would benefit from working with us, we’re more than happy to have a confidential chat with them.

SHARE THIS POST

Why Use a Financial Adviser When Investing

A financial advisor can provide the perspective investors need to tune out the daily noise and stay focused on a long-term plan. Check out this video about why using a financial planning professional can give you peace of mind and ensure you stay on track to achieve your goals, and not be distracted by the ups and downs of the stock markets and media hype around the economy.

Click the link below for the video

The Difference the Right Financial Advisor Makes (dimensional.com)

SHARE THIS POST

Six Simple Mind Tricks For Dealing With Uncertainty

It may feel like we are living in extremely uncertain times, and that we now lack control over many important things in our lives, but is it still possible to be happy?

Here are six tips from experts in psychology and neuroscience on how to better manage the uncertainty in your life during these unprecedented times.

https://www.bbc.com/reel/video/p08bmr62/six-simple-mind-tricks-for-dealing-with-uncertainty

SHARE THIS POST

Compound Interest: What Every Investor Needs to Know

Compound interest is one of the most important things that an investor can understand. In this video, financial journalist NORMA COHEN explains how fundamental the concept is to successful investing – as well as the potential drawbacks that investors need to be aware of.

https://www.evidenceinvestor.com/compound-interest-what-you-need-to-know/

© The Evidence-Based Investor MMXXIV

SHARE THIS POST

Why work with a REAL Financial Planning adviser? And how do you know who to choose?

Many people think they need to have a large lump sum of money to invest before seeking advice from a financial adviser, however, this is not necessarily true!!

There are many types of financial advisers – investment adviser, mortgage adviser, insurance adviser, all coming under the name of ‘Financial Adviser’, so be sure you understand what their expertise is, before you engage their services – they need to fit with what you want and need.

When it comes to PLANNING however, where you want someone who has experience in a whole range of financial matters that we come across in our lives, such as paying off debt alongisde investing too, saving for your children’s future and your own retirement, where to invest your money (property, shares or both), how to ensure you have the right ownership structures in place (individually, jointly, in a Trust or your business), safeguarding your wealth and income with the best personal insurance and ACC solutions, and protecting your hard earn assets through Wills, Enduring Powers of Attorney and Trusts, you need the expertise of a FINANCIAL PLANNER.

A FINANCIAL PLANNER, especially a Certified Financial Planner CFPcm , is an expert who has the skills, qualifications and experience to cross all these arenas and provide you with holistic advice and ongoing guidance, giving you peace of mind, security, and someone you can use as sounding board when times are tough. They want to know who you really are and what’s important to you, so they can help you make informed decisions on how to ‘get ahead’ and save you from making any big mistakes that may ‘set you back’ financially.

Look for a Certified Financial Planner CFPcm who enjoys working across all areas of your financial life and wants to build a long term relationship with you, loves sharing knowledge and ideas yet will challenge you when needed, and will keep you on track to living your best life!

Jane Benton & Charlene Overell

G3 Financial Freedom Ltd

Certified Financial Planners CFPcm / Acredited Investment Fidudiaries AIF®

SHARE THIS POST

Let’s Talk Legacy: Engaging the Family in Financial Planning for the Next Generation

We hope this message finds you well and in good spirits as we approach the holiday season. As we gather together to celebrate our shared traditions, we wanted to propose a meaningful conversation that goes beyond the usual festive cheer.

We believe it’s time for us all to come together and discuss something equally important—our family’s financial future. It’s a topic that may not have been in the forefront of our conversations, but addressing it collectively could make a significant impact on the generations to come.

Here are a few thoughts on how we can all engage in meaningful financial planning discussions:

- Family Financial Gathering: Consider organising a family financial gathering during the holidays or another convenient time. This could be an informal get-together where everyone can share their individual financial goals, challenges, and dreams. Creating an open space for conversation can be enlightening and foster a sense of shared responsibility.

- Educational Sessions: To ensure that everyone is on the same page, why not arrange for educational sessions on financial planning. These sessions could cover topics like budgeting, investing, saving for education, and retirement planning. Bringing in a financial planning professional to guide everyone through these discussions could provide valuable insights tailored to your family’s unique needs.

- Setting Family Financial Goals: Collectively set financial goals for your family. Whether it’s saving for a significant event, creating an emergency fund, or planning for future generations, having clear objectives will guide your financial decisions and create a sense of purpose.

- Teaching Financial Literacy: Consider incorporating financial literacy into your family traditions. For instance, this could involve the younger members in budgeting discussions or sharing stories about financial successes and lessons learned. By instilling financial literacy early on, we empower the next generation to make informed decisions.

- Legacy Planning: Discussing your family legacy can be a powerful motivator for financial planning. Whether it’s passing down financial values, creating a family foundation, or ensuring a smooth transition of assets, planning for our financial legacy can bring a sense of continuity and purpose.

- Celebrate Milestones: Acknowledge and celebrate financial milestones within the family. Whether it’s paying off a significant debt, achieving a savings goal, or making a wise investment, recognising and celebrating these achievements fosters a positive financial culture within the family.

- Encourage Questions and Involvement: Create an environment where everyone feels comfortable asking questions and actively participating in financial discussions. By fostering an open dialogue, we can collectively learn from each other and make informed decisions.

We believe that by engaging in these conversations, we can lay the foundation for a financially secure and thriving family. Let’s embark on this journey together and make financial planning an integral part of our family legacy.

Please feel free to reach out to us if you’d like assistance with you and your family considering any of these ideas.

Charlene Overell

G3 Financial Freedom Ltd

SHARE THIS POST

“Cooking Up Success: Crafting Your Financial Recipe for a Prosperous Future”

Just as a chef meticulously selects ingredients to create a masterpiece in the kitchen, achieving financial success requires careful planning and a strategic recipe. In the realm of personal finance, consider yourself the chef, and your financial goals the delectable outcome. In this article, we will explore the key ingredients and steps to concocting your financial recipe for a prosperous future.

- Define Your Financial Goals: Just as a chef starts with a vision of the dish they want to create, begin your financial journey by clearly defining your goals. Whether it’s purchasing a home, retiring comfortably, or starting a business, having a clear picture of your objectives is the first step in crafting your financial recipe.

- Create a Budget – The Foundation of Your Recipe: A budget is the financial foundation upon which success is built. Similar to measuring ingredients in a recipe, create a detailed budget that outlines your income, expenses, and savings goals. Knowing where your money is going allows you to make intentional decisions about how to allocate resources.

- Save and Invest – The Building Blocks of Wealth: Just as a chef carefully selects premium ingredients, be intentional about saving and investing. Set aside a portion of your income for savings and explore investment opportunities that align with your goals. Investments act as the building blocks of wealth, providing returns that can grow over time.

- Diversify Your Portfolio – Mix it Up: In the world of finance, diversification is akin to mixing different flavours to create a balanced dish. Diversify your investments across various asset classes to spread risk and enhance potential returns. A well-mixed portfolio can weather economic fluctuations and provide stability.

- Debt Management – Balancing Flavors: Just as a chef balances flavours in a dish, managing debt is about finding the right equilibrium. Prioritize high-interest debts and work towards paying them off. Consider consolidating or refinancing to achieve a more favourable balance in your financial flavours.

- Continuous Learning – The Seasoning of Success: Successful chefs are always learning and experimenting with new techniques. Similarly, financial success requires continuous learning. Stay informed about market trends, financial tools, and opportunities. This ongoing education adds seasoning to your financial recipe, enhancing its flavour over time.

- Emergency Fund – The Safety Net: Every chef has a contingency plan in case something goes wrong. Similarly, build an emergency fund as your financial safety net. Having three to six months’ worth of living expenses set aside provides peace of mind and ensures you can weather unexpected financial storms.

- Insurance – Protecting Your Recipe: Just as chefs use lids and covers to protect their creations, insurance safeguards your financial recipe. Ensure you have adequate health, life, and property insurance to protect against unforeseen events that could potentially disrupt your financial stability.

- Review and Adjust – Taste Testing Your Recipe: Successful chefs taste their creations throughout the cooking process. Similarly, regularly review your financial recipe. Assess your progress towards goals, adjust your budget as needed, and reallocate resources based on changing circumstances. This active involvement ensures your financial recipe stays on track.

- Seek Professional Advice – Consulting the Master Chef: Just as aspiring chefs seek guidance from master chefs, consider consulting with a financial planning adviser. A seasoned professional can provide insights, strategies, and guidance tailored to your unique financial palate, especially when you may only have time to create small parts of the financial dish yourself, needing an expert who can add their creative knowledge to better the end result.

Conclusion:

Creating a financial recipe for success is an art that requires patience, dedication, and careful planning. By defining your goals, budgeting, saving, and investing wisely, you can craft a recipe that leads to a prosperous and fulfilling financial future. Much like a well-prepared dish, your financial success will be the result of thoughtful preparation, attention to detail, and a dash of creativity. Bon appétit!

Charlene Overell

G3 Financial Freedom Ltd

SHARE THIS POST

Investing During Inflationary Times – Does A Term Deposit Really ‘Cut It’

So, what is inflation? Investopedia describes it as “a rise in prices, which can be translated as the decline of purchasing power over time”.

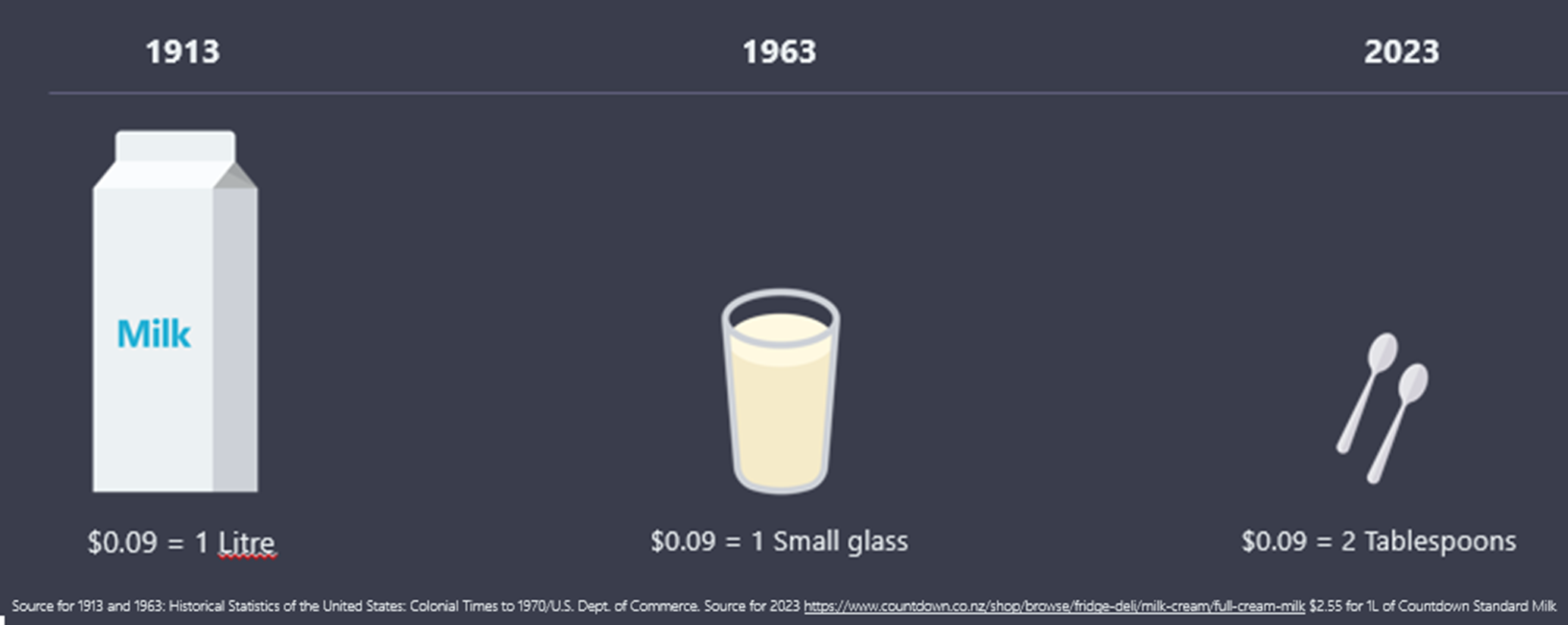

Let’s have a look at the price of a cup of black filter coffee over time:

And the price of milk back in 1913 was $0.09 for 1 litre, which in 1963 would have bought you 1 small glass and today in 2023, would buy you 2 tablespoons!!

The inflation tax, by Warren Buffet:

“It makes no difference to a widow with savings in a 5% (term deposit) whether she pays 100% income tax on her interest income during a period of zero inflation or pays no income tax during years of 5% inflation. Either way, she is ‘taxed’ in a manner that leaves her no real income whatsoever. Any money she spends comes right out of capital. She would find outrageous a 100% income tax but doesn’t seem to notice that 5% inflation is the economic equivalent”.

Inflation erodes cash’s value

It appears that now, whilst bank savings interest rates are higher than they were a few years ago, there is a view by some people, that leaving money in cash in the bank, maybe within a term deposit account, is the best option to help grow their money, or at least leave it there whilst they feel the share markets or the economy will get better. Unfortunately this is a misconception. Whilst cash is good for short term savings for specific items, maybe a holiday, car, wedding or home deposit, and especially for emergency purposes, cash is not ideal for growing wealth for the long term. One of the most significant drawbacks of investing in cash is that it fails to keep pace with inflation

If we can receive a term deposit rate of say 6% pa (gross, so before tax), and inflation is running at 7%, then we have already lost 1% of its value in a year, meaning what we can buy today for our money, we will not be able to buy next year. If we are paying tax at the 30% rate too for example, then the rate after tax (net) is 4.2%. Turning this into dollars, if we invest $100,000 in that same term deposit account, then after 30% tax the interest earned at the year end is $4,200. However, whilst we still have the $100,000 in our account, as inflation was 7%, and we only earned 4.2% after tax, then this capital value has gone backwards in real terms to $97,200……..meaning that what we could have bought for $100,000 the previous year, is going to cost us $102,800 this year.

If we continue to invest in cash with the illusion that our capital will remain intact, then whilst on paper it will, in real terms it will not. Just compound the above example over many years and we can see how the value is being eroded year on year by inflation.

Diversification reduces risk

Thinking about what we want from our money in life, now, and over the medium and longer term, is the key, and then having our money allocated to different ‘buckets’ will support our spending needs throughout the rest of our life.

So yes, whilst cash is good for the short term savings we need for specific items and for a ‘rainy day’, having a well-diversified portfolio of shares and bonds will help to keep pace with inflation, grow wealth, and ensure there will be enough to pay the bills and enjoy the life we want over the next 10+ years.

Historically, the average annual return on the stock market, adjusted for inflation, has been significantly higher than the return on cash investments. Shares have the potential to provide us with the capital appreciation needed to grow wealth and maintain its value in the face of rising prices.

Investing solely in cash exposes our wealth to significant risks, such as economic downturns, changes in interest rates, and unexpected expenses that erode the value of our cash. Building a well-diversified portfolio, which typically includes shares and bonds from various industries, sectors and across the world, will reduce this risk. Diversifying worldwide also helps protect our investments from the impact of a single company’s poor performance or a specific economic downturn. Even during market fluctuations, the broader market tends to recover over time, reducing the risk of losing our entire investment.

Property vs shares

Property, like shares, is a growth asset and has historically shown to outperform cash over the longer-term too. However, whilst investing in property provides a rental income for those wanting income, or a potential capital growth in the future, we need to be careful that this income return is actually a good one for the risk we take, after taking account of all expenses for running the property and tax we have to pay. A capital gain can be achieved, however, we need to be mindful of what this gain may be after taking account of all costs during the term of holding it.

The downside of property is that if we need money for a specific spend, then we cannot ‘carve’ a lump sum of cash off of the side of our property, meaning it is illiquid. We would have to wait to sell it to release the cash value, or be forced to sell it (which may be not ideal depending upon property values). Holding a well-diversified quality share portfolio means we can release money when we need it, as this is liquid and shares/bonds can be sold pretty much straight away. Having a combination of both property and shares may be ideal depending upon your goals.

Conclusion

Whilst cash has its place in a well-rounded financial strategy, relying on it solely as an investment vehicle can hinder your long -term financial goals. The erosion of purchasing power due to inflation, limited returns, and the absence of compounding, makes cash less than ideal for wealth creation.

If you come into wealth suddenly, through the sale a property, a business, or an inheritance, then of course put this into cash in the bank temporarily – this will give you time to breath and to seek independent financial planning advice from an expert adviser who can carefully consider your risk tolerance and tailor a plan to suit your goals and tax position. Although shares come with their own set of risks, a well-managed portfolio can help you build wealth and achieve your financial objectives over time.

Charlene Overell 16.09.23

SHARE THIS POST

UK Supreme Court Delivers Milestone Judgement On A Bank’s Duty To Follow Customer Instructions

The United Kingdom’s Supreme Court has delivered an important judgement holding that where a customer has unequivocally authorised and instructed its bank to make a payment, the bank must do so and is not under any obligation to make further enquiries. This article from Bell Gully shares how they expect this judgment to be influential on New Zealand courts.

Sophie East and Jack Worthington

The United Kingdom’s Supreme Court has delivered an important judgment holding that where a customer has unequivocally authorised and instructed its bank to make a payment, the bank must do so and is not under any obligation to make further inquiries1.

This provides a refinement of what was previously referred to as the ‘Quincecare’ duty. In making this finding, the Supreme Court provides a helpful analysis of the agency relationship between a bank and a customer, and makes special mention of the scholarship of New Zealand academic, Professor Peter Watts. We expect the judgment to be influential on New Zealand courts.

Facts

The case concerned a couple, Dr and Mrs Philipp, who fell victim to a type of fraud known as “authorised push-payment” (APP) fraud. This is when an individual authorises their bank to send a payment of monies to a bank account that is controlled by a fraudster. In this case, Dr and Mrs Philipp were contacted by an individual claiming to working for the Financial Conduct Authority in conjunction with the National Crime Agency. Through a series of communications, Dr and Mrs Philipp were led to believe that they needed to move their money to a “safe account” to protect their funds. Acting on the advice of the fraudster, the Philipps went to a branch of Barclays Bank where they gave instructions for an international payment to be made from their bank account to an account in the United Arab Emirates. As a result of the fraud, a total of GBP700,000 in two payments were made to the fraudster’s bank account, and was unable to be recovered by the bank.

Mrs Philipp brought proceedings against Barclays for what she claimed was a breach of the duty of care that the bank owed her as a customer. In reliance on what is known as the Quincecare duty of care, Mrs Philipp argued that the bank was under an implied common law duty to refrain from executing her instructions as it had reasonable grounds for believing that the order was an attempt to misappropriate her funds. In reply, Barclays applied for summary judgment that the claim be dismissed on the basis that the bank did not owe Mrs Philipp such a duty.

The High Court agreed with the bank, and summary judgment was awarded in favour of Barclays. This decision was then successfully appealed by Mrs Philipp to the Court of Appeal. The Court of Appeal found that the bank does owe a contractual duty to its customers, as outlined in Quincecare, and whether such a duty exists on the facts in this case was to be decided at trial. In turn, Barclays appealed this decision to the Supreme Court.

What is the Quincecare duty?

The Quincecare duty, from the judgment of Steyn J in Barclays Bank plc v Quincecare Ltd2, requires a bank to make inquiries about the validity of a customer’s instruction if it has reasonable grounds for believing that the instruction is induced by fraud and would result in the misappropriation of the customer’s funds. This duty, which has been cited positively by New Zealand courts3, had previously only applied to cases where agents were engaging with the bank purportedly on the instructions of a customer. However, the English Court of Appeal in the Philipp case found that the duty also extended to circumstances where the bank has received instructions from the customer directly. That was the issue on appeal to the UK Supreme Court.

UK Supreme Court judgment

The Supreme Court rejected the argument that the Quincecare duty should extend to cases where a customer has given direct instructions to the bank to make a payment. On behalf of the Court, Lord Leggatt highlighted the basic and strict duty of a bank under its contract with a customer to make payments from the customer’s account in compliance with the customer’s instructions. In other words, “it is not for the bank to concern itself with the wisdom or risks of its customer’s payment decisions.”4 In emphasising the strict nature of this duty conferred on banks, the Court cited Westpac New Zealand Ltd v MAP & Associated Ltd where the New Zealand Supreme Court found that even when a bank has reasonable concerns that it might incur legal liability by carrying out a customer’s payment instructions, this is not enough to afford the bank a defence to a refusal to carry out instructions (rather, the bank must show it would have actually incurred liability)5. For Dr and Mrs Philipp, because they gave direct instructions to the bank to make the two payments totalling GBP700,000, there is no question as to the validity of the instruction that was given to Barclays. Any refusal by the bank to carry out this instruction would be a breach of duty by the bank.

Thus, the UK Supreme Court in Philipp confined the Quincecare duty on banks to make inquiries to a specific type of situation (where instructions are made via an agent and give grounds for suspicion), but held this does not apply to direct instructions from a client itself (which the bank is obligated to carry out).

What is particularly interesting about the Supreme Court judgment is its discussion of the role of the court versus the legislature. The Supreme Court acknowledges that the type of fraud that Dr and Mrs Philipp fell victim to is a growing social problem. However, it states that “whether victims of such frauds should be left to bear the loss themselves or whether losses should be redistributed by requiring banks which have made or received the payments on behalf of customers to reimburse victims of such crimes is a question of social policy for regulators, government and ultimately for Parliament to consider.”6

Comment

In New Zealand, our Supreme Court has already held in Westpac v MAP that banks are under a strict duty to comply with legitimate payment directions made by their customers. Absent a provision in the bank’s terms that permits some other approach, banks generally do not have a discretion as to whether or not to make a payment. This gives customers confidence that their directions will be followed, and allocates responsibility firmly with the customer that gives the instruction. The Philipp case is likely to be a further barrier to claims in New Zealand against banks by customers (or others) seeking to recover losses arising from the execution of legitimate payment directions.

If you have any questions about the matters raised in this article, please get in touch with the contacts listed at the start of this article or your usual Bell Gully adviser.

[1] Philipp v Barclays Bank UK PLC [2023] UKSC 25.[2] Barclays Bank plc v Quincecare Ltd [1992] 4 All ER 36.[3] See, e.g., Tandem Group Limited v ASB Bank Limited [2021] NZHC 51 at [31] to [37].[4] Philipp at [3].[5] Westpac New Zealand Ltd v MAP & Associated Ltd [2011] NZSC 89, [2011] 3 NZLR 751.[6] Philipp at [6].

SHARE THIS POST

There’s No Time Like The Present – The Importance Of Wills And Enduring Powers Of Attorney

Wills and Enduring Power of Attorney documents are among the most important legal documents, but are often overlooked. Everyone from as young as eighteen should have these documents for the reasons set out below.

Wills

Why is a Will important

A Will sets out a person’s wishes after they die and appoints a person or persons called executors to be legally responsible for carrying out these wishes. It often comes as a surprise to New Zealanders that if you do not leave a Will recording how you would like your assets to be distributed, then the Administration Act 1969 (“the Act”) will decide for you.

What happens if you die without a Will

Someone (generally a family member) then must apply for Letters of Administration if the estate is valued over $15,000 and ask to be the administrator of the estate. This process can be more costly in comparison to that involved when the deceased has left a valid Will.

The application is made to the High Court and can take some time to be processed. The administrator then has full authority to distribute the assets in accordance with the Act which dictates who is to receive the deceased’s personal chattels and balance of assets. The Act’s order of priority may not align with your wishes. By way of example, in the case of a surviving spouse and children:

- the spouse receives:

- All of the deceased’s personal belongings.

- A set dollar amount which is currently $155,000, plus one-third of the rest of the deceased’s estate (i.e. home, KiwiSaver, personal bank account balances).

- The children receive the other two-thirds of the deceased’s estate in equal shares.

Matters to consider

If you do not have a Will or have not updated your Will for some time, you should consider the following:

- Who would I trust to be responsible for my assets when I pass?

- Who do I want to ensure is looked after when I pass?

- Do I have any special items that I want to give to particular people?

- Do I want to set up a Trust when I pass or gift money or property to an existing Trust?

- Do I want to support a charity or community organisation?

- What is to happen with my Māori Land interests?

- Who will look after my infant children when I pass?

- What funeral arrangements would I prefer?

Enduring Power of Attorney

What is an Enduring Power of Attorney

Enduring Power of Attorney (“EPA”) documents are equally as important as Wills. They protect you and your family in the event that you lose mental capacity (which could be as a result of an accident or medical condition). These documents authorise particular persons to step in and manage your affairs during your lifetime.

There are two types of EPA:

- EPA in respect to property – Management of your personal finances and property.

- EPA in respect to personal care & welfare – Decisions round wellbeing including where you live and how you will be cared for.

You require two documents (one for each type of EPA) in order to cover all circumstances.

What happens if you lose mental capacity without having EPA documents in place

In the absence of EPAs, your loved ones would be faced with having to apply to the Family Court for the appointment of a property manager and welfare guardian. This can be a lengthy and costly process for loved ones who are already in a stressful situation.

Matters to consider

- Who do I trust to make decisions in respect to my wellbeing?

- Who do I trust to manage my personal finances and assets?

- Who do I wish to appoint as a back-up attorney?

- Do I want my attorney to consult another person or persons?

- Do I want my attorney to provide another person or persons with information?

- Do I want to impose any conditions?

Next Steps

Holland Beckett Law can assist with all of your estate planning needs. There is no time like the present, so please reach out to get your estate planning underway.

Brittany Ivil

Associate

07 928 7098

Brittany.Ivil@hobec.co.nz

SHARE THIS POST

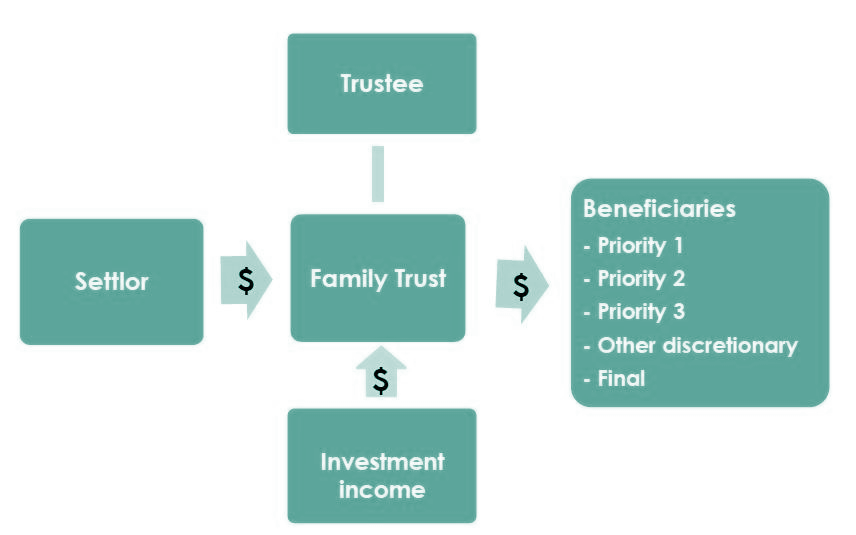

What Does The New Trustee Tax Rate Mean For You?

As part of the Budget earlier this year, the Government surprised us with an announcement that it would raise the tax rate on Trusts from 33% to 39%, effective from 1 April 2024. For a Budget which was badged as having ‘no major tax changes’, this felt like a major change for the 400,000 Trusts registered in New Zealand.

This change brings the trustee tax rate into alignment with the highest personal income tax rate; and in line with Australia, Canada, the United Kingdom, and the United States who all align their trustee tax rates with top personal tax rates.

The rationale was a spike in the amount of income being put through Trusts, rising by $5.7b, or almost 50% from $11.4 in the 2020 tax year to $17.1b in 2021. The Government expects to raise a further $350m in tax per year following this change.

Will this change impact all Trusts?

Many Trusts will be used solely to own a family home and possibly a bach, so will be inactive for tax purposes and not affected at all.

The target for this increased Trust tax rate is wealthy individuals who invest, earn and retain wealth within Trusts which currently pay a flat 33% tax on income generated.

In the middle are many family Trusts that generate income from money invested in bank deposits, fixed interest, shares, and property investments. For those trusts that distribute the income to beneficiaries on lower tax rates, there will be no change. However, those that reinvest earnings within the Trust are likely to suffer collateral damage and will end up paying the higher tax rate.

Each year, accountants review income generated by Trusts and beneficiaries to determine how best to treat the income – either a) allocate it to beneficiaries and pay tax at their personal rates, or b) retain it within the Trust and pay tax at the trustees tax rate.

In making this decision, accountants and trustees consider various factors including:

- actual distributions made during the last year

- payments expected in the year ahead

- tax credits available

- expenses or losses to be claimed, as well as

- the best treatment for tax purposes

To illustrate, here is a simplified example:

ABC Trust has an investment portfolio and two main beneficiaries, Mr and Mrs Smith. Gross taxable income generated during the year was as follows:

- ABC Trust $ 15,000.00

- Mr Smith $ 30,000.00

- Mrs Smith $ 55,000.00

At the end of the tax year, the trustees can choose how to allocate that income. Each option results in different levels of tax payable on that income, as illustrated below:

- Retain the income with the Trust = $15,000.00 x 33% = $5,000.00 tax

(This would rise to $5,850.00 under the new 39% trustee tax rate)

- Distribute the income to Mr Smith = $15,000.00 x 17.5% = $2,625.00 tax

- Distribute the income to Mrs Smith = $15,000.00 x 30% = $4,500.00 tax

In the above example, the most tax effective option would be to allocate and distribute income to Mr Smith as he has the lowest taxable income and marginal tax rate (17.5%).

Are there any exceptions?