The poor plight of investors that switched from Term Deposits during COVID

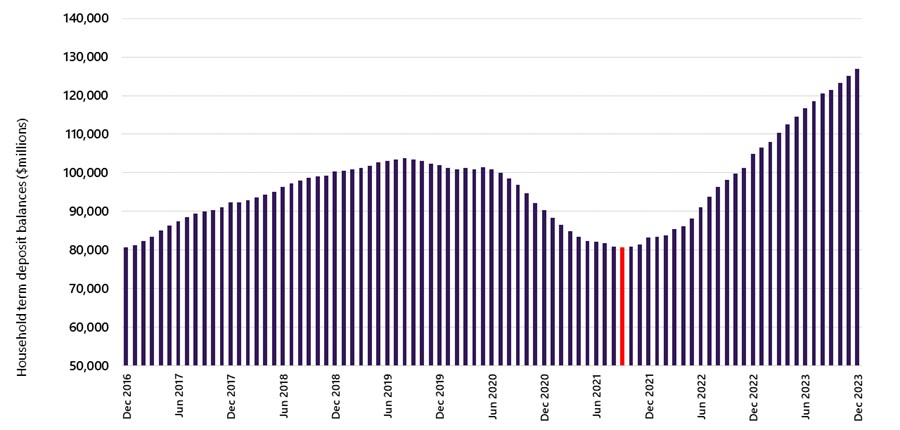

It’s a little detail you may have missed, and even if you heard it, you probably gave it no more than passing attention. In December 2023, New Zealand hit an all-time high in term deposit (TD) balances of a whopping $213b1. If you look only at households (see the chart below), that number reached $127b, easily outstripping the combined balances of every KiwiSaver investor in the country.

While that huge number is interesting, what’s more interesting is the change of TD balances over time. It turns out that TD balances have not experienced a slow and steady upward climb. Instead, there was a recent peak, followed by a trough, and now we are on another peak. The low balance point, September 2021, is highlighted in red.

Household TD’s and NZX50 Growth of Wealth Dec 2016 – Dec 2023

Source: RBNZ and NZX

This chart shows that investors were slowly accumulating TD assets from 2016 to 2019. Then, in response to COVID, the Reserve Bank sharply reduced interest rates. Pretty soon, about $25b in TD assets started looking for something (anything) with a higher yield. At the time, investment portfolios looked like an attractive alternative based on the recent good run the market had experienced.

By December 2022, the trend (and interest rates) had reversed, and TD balances were back to setting all time highs which continued unabated in 2023.

So, what is the issue?

The issue is the remarkably bad investment timing this represents and impact it likely had on many new investors.

From 2016 – 2019 whilst TD volumes were growing steadily, the New Zealand share market measured by the NZX 50 Index (Gross) generated, on average a return of 16.10% per year. By comparison 6-month TD’s generated 3.25% per year over that same time period. Despite these unusually good share market returns, TD balances were gradually still increasing each month. In other words, TD investors were not noticeably substituting out of TDs and moving into those high performing assets during the years of great share market results.

But investors, at least anecdotally, did decide to switch from TDs to investment portfolios throughout 2021 and 2022 and TD balances hit their low point in September 2021. In other words, for investors that moved away from TDs, the date of their maximum exposure to investment markets was September 2021. Unfortunately, from that date to the end of 2022, the NZX50 returned an unwelcome -10.08% and the NZX Investment Grade Corporate Bond Index delivered -5.31%.

Following that uncomfortable investment experience, investors apparently came rushing back into TDs. And, while they did, markets recovered. Sure, the NZX was up only 2.59% in 2023, but the bond index was up 7.54% and the MSCI All Country World Index (gross div.) was up 23.35% helping investors that diversified internationally.

So, here’s the problem in a nutshell:

- A large group of TD investors appear to have missed out on the great investment markets pre-COVID.

- Disenchanted with low interest rates, they moved into investment portfolios in 2021 and 2022 searching for better returns.

- They ended up running right into bad share returns and historically bad bond returns.

- Many appear to have jumped back out of investment markets in 2023 only to miss out on the stellar bond and global investment returns that 2023 delivered to disciplined investors.

Yikes!

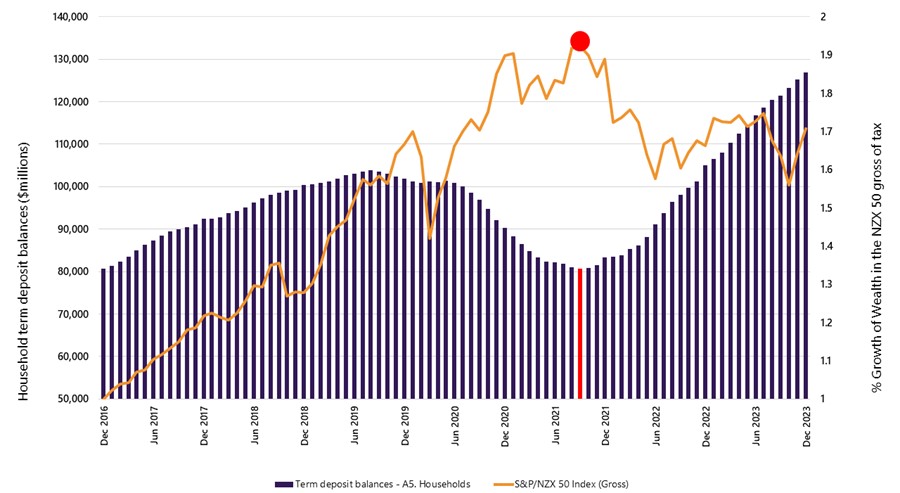

The graph below really shows the story. TD deposits hit their lows, right on cue when the NZX hit its high (September 2021). So, as markets go down, the maximum amount of former TD investors feel the brunt of poor returns, and they quickly move back into TD’s rather than stick around to enjoy the recovery.

We’ve highlighted September 2021 when the NZX50 was at its peak and the cumulative TD balance was at its low (the same month).

Household TD’s and NZX50 Growth of Wealth Dec 2016 – Dec 2023

Source: RBNZ and NZX

What is the lesson?

The first lesson is that as a nation we are collectively terrible at ‘timing’ markets. But we’re not alone.

In the United States one of the most esteemed investment consultants is Charles Ellis, author of “Winning the Loser’s Game.” He said this about market timing, “market timing is a truly wicked idea. Don’t try it.”

He also said, “Market timing is unappealing to long-term investors. As in hunting deer or fishing for rainbow trout, investors have learned the importance of ‘being there’ and using patient persistence – so they are there when opportunity knocks.”

For investors that started investing in 2021 only to be disappointed in 2022, our strong encouragement is to hold on and stay disciplined. It’s nearly impossible to pick the times to be in and out of the market. Instead, if their strategy needs to last over decades, then give it time and work with an adviser to see if the plan is still on track, or if they need to make some small adjustments.

Discipline and time are the super skills of great investors. It’s the one thing consistently rewarded, and something that a good adviser can help us be much better at.

1Source: Banks: Liabilities – Deposits by sector (S40) – Reserve Bank of New Zealand – Te Pūtea Matua (rbnz.govt.nz)

Ben Brinkerhoff

Consilium

08 April 2024